")

Night Time Weight Loss Pills for Women – Advanced Weight Loss Supplement – Fat Burners for Women – Diet Pills that Work Fast – Belly Fat Burner – Appetite Suppressant – Made in USA")

Thank you for reading this post, don't forget to subscribe!

TradingKey – March 31, ET, Eli Lilly (LLY.US) officially announced that it will acquire the U.S.-listed company for a total consideration of $7.8 billion Centessa Pharmaceuticals (CNTA.US) , with the transaction expected to close in the third quarter of 2026. Following the news, Eli Lilly shares rose approximately 3% on Tuesday, while Centessa shares surged 45%.

[Source: Google Finance]

Centessa Pharmaceuticals (CNTA.US) primarily develops innovative drugs to treat neurological disorders such as narcolepsy, Alzheimer’s disease, and depression, and may even have broader applications.

Under the terms of the agreement, Eli Lilly will pay an upfront price of $38 per share, or $6.3 billion, to acquire Centessa, representing a 38% premium over Monday’s closing price. Eli Lilly will pay up to an additional $1.5 billion if Centessa’s drug receives U.S. Food and Drug Administration (FDA) approval by a specific deadline.

Notably, year-to-date, Eli Lilly has announced plans to acquire cell therapy company Orna Therapeutics and inflammation-focused Ventyx Biosciences.

Compared to Novo Nordisk, Eli Lilly has maintained a lead in the weight-loss drug sector in recent years and continues to broaden its advantages in other fields.

Dr. Carol Ho, President of Lilly Neuroscience, stated in a statement, “Centessa has a portfolio with both breadth and depth that can improve wakefulness across a wide range of indications.”

The pharmaceutical giant has a market capitalization of $820 billion. Despite strong revenue growth of 45% over the past 12 months, its stock price has fallen 17% year-to-date.

[Source: TradingKey]

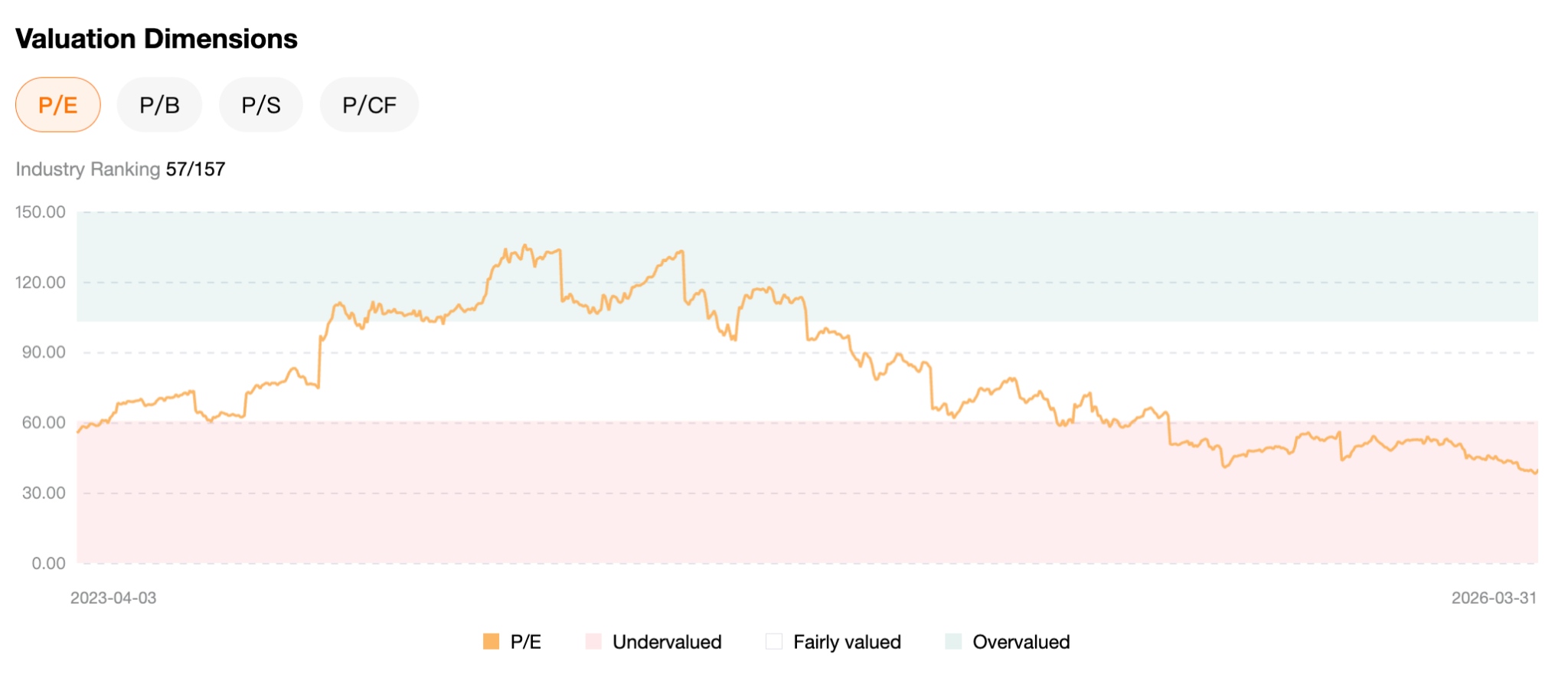

Given its rapid growth challenging Novo Nordisk’s dominance in the weight-loss drug market, and considering its current P/E ratio, we believe there is still significant room for future growth.

[Source: TradingKey]

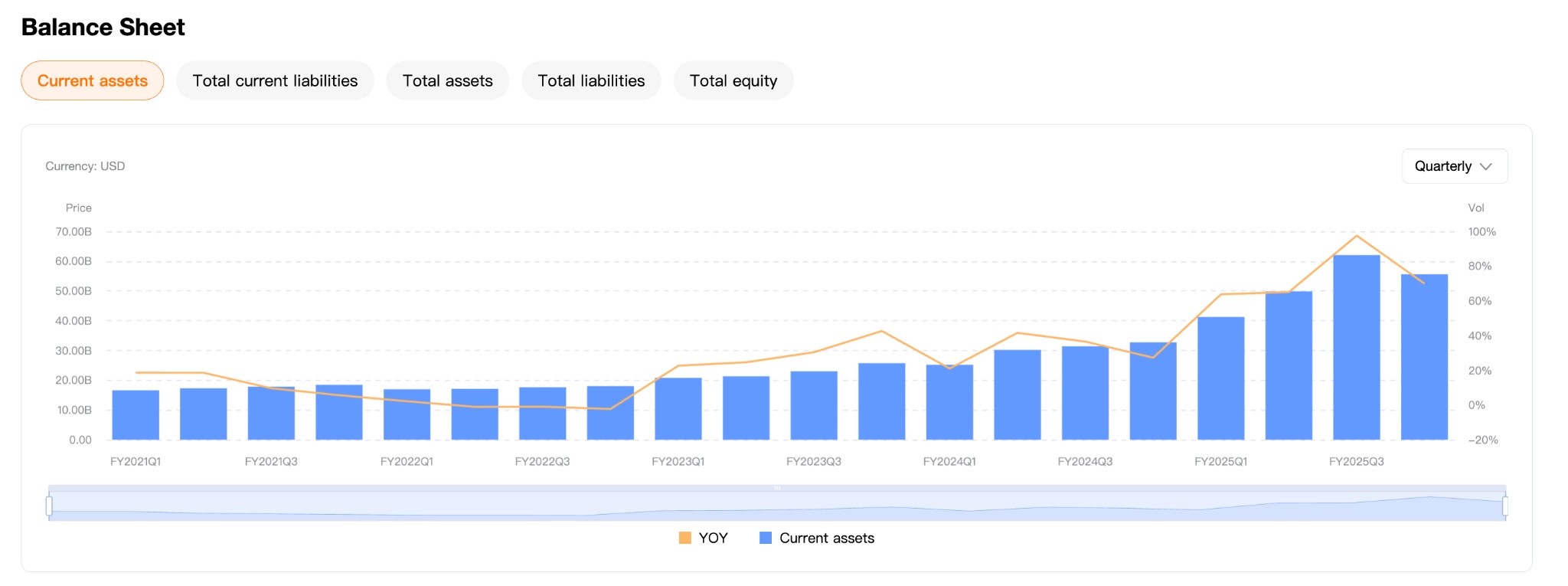

Regarding cash flow, Eli Lilly’s cash flow has continued to increase since 2022. The company possesses ample cash flow for acquisitions and R&D investment; cash flow serves as an indicator of whether a company’s fundamentals are stable.

[Source: TradingKey]

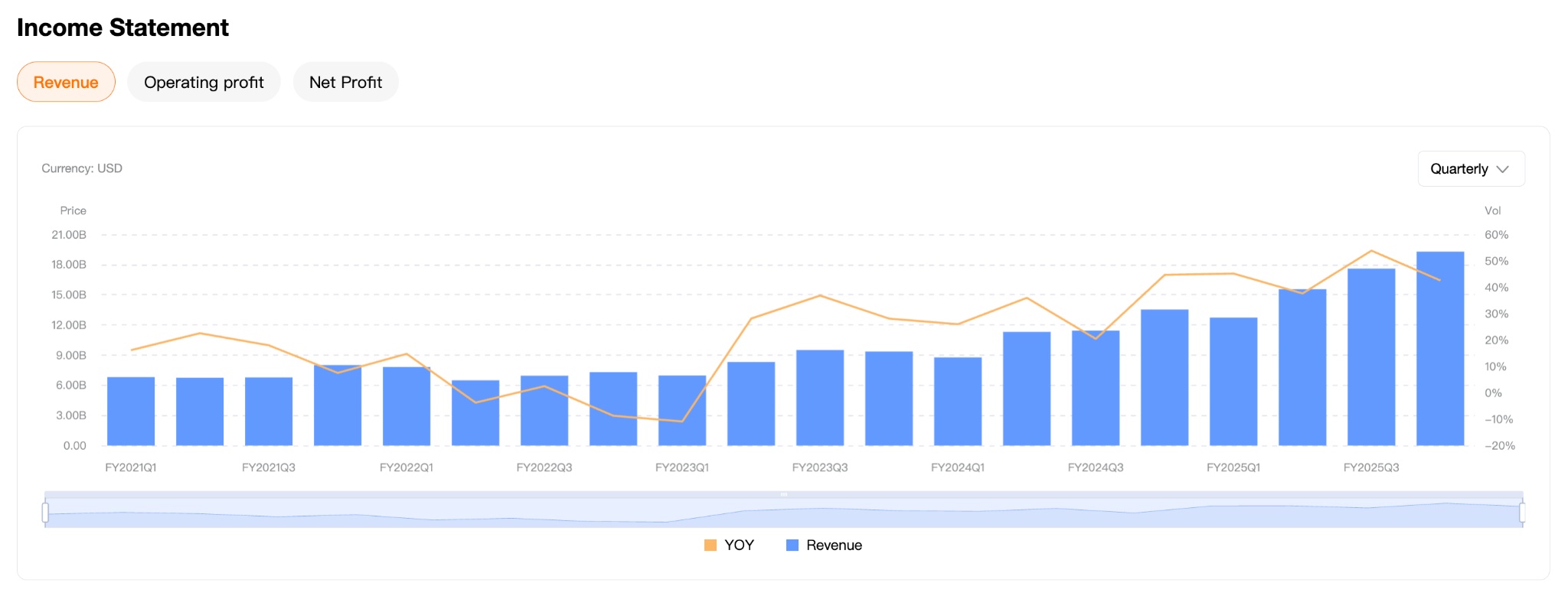

In terms of revenue, Eli Lilly’s top line has continuously increased since 2023 due to market expansion. The substantial revenue growth demonstrates the strength of its business, and there are currently no signs of a slowdown.

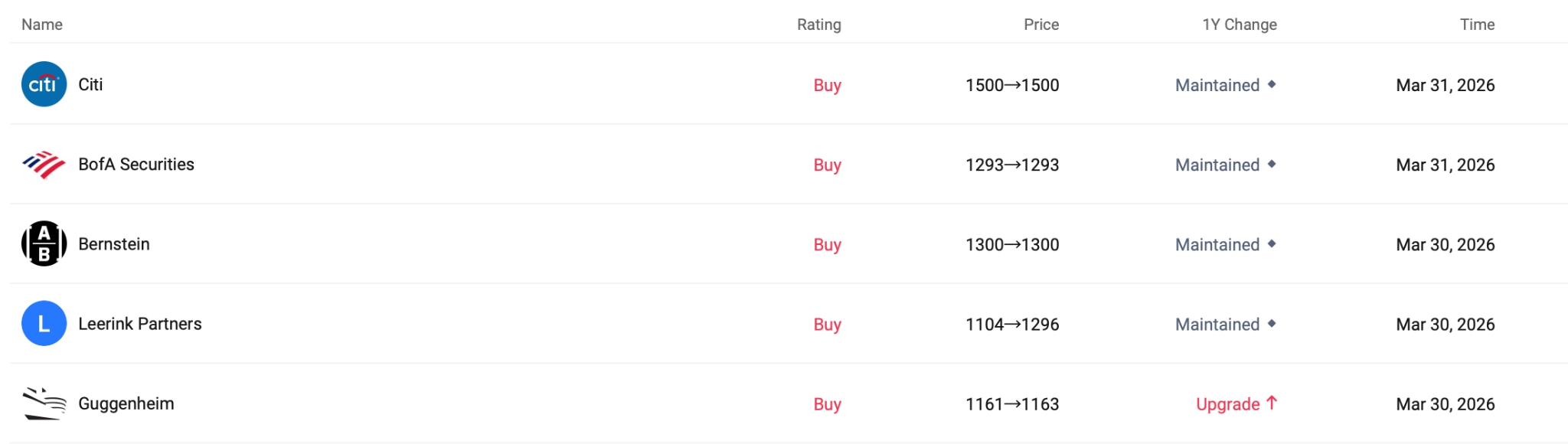

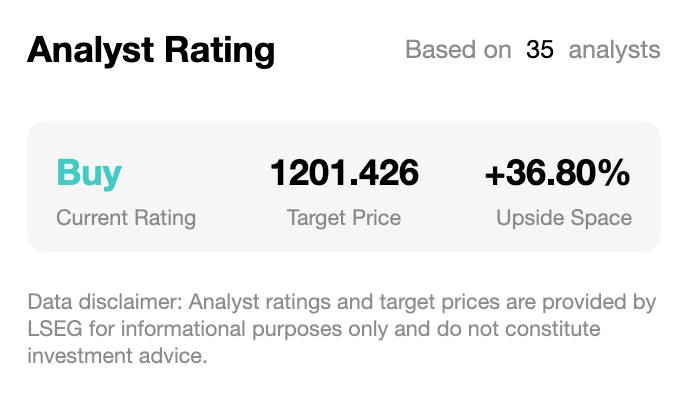

From an institutional perspective, most firms maintain a Buy rating on Eli Lilly. TradingKey data indicates that the potential upside for Eli Lilly’s target price range remains at 36.8%.

[Source: TradingKey]

Meanwhile, Barclays reiterated its Overweight rating on Eli Lilly stock (NYSE: LLY) and maintained a $1,350 price target following news of the deal.

Barclays considers the transaction a complementary acquisition for Eli Lilly’s neuroscience division. The company is expanding its pipeline beyond neurodegenerative indications, including brenipatide, which is currently in Phase 3 clinical trials for the treatment of alcohol use disorder and major depressive disorder.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Source link